IEEPA Tariff ruled unconstitutional

The Supreme Court ruled on Friday that the IEEPA tariff (International Emergency Economic Powers Act) is unconstitutional.

CBP published official guidance on the evening of February 22 confirming that as of February 24, the IEEPA tariff is void. It will not apply to any entries going forward.

Section 122 – The Replacement Tariff

In the wake of the IEEPA ruling, the President has enacted Section 122 of the Trade Act of 1974, citing monetary imbalances with other nations. This provision allows a temporary import surcharge of up to 15% for up to 150 days, without congressional approval.

The rate is 10%, though the President has threatened to raise it to 15%. As of the time of this writing, the official White House action still reflects 10%. You can read the full presidential action here:

White House Section 122 Presidential Action

What Is Excluded from Section 122?

The following goods are excluded from the 10% Section 122 surcharge:

• Goods loaded onto a vessel destined for the U.S. before February 24, 2026, and arriving or withdrawn from warehouse before February 28, 2026

• Aircraft and aircraft parts

• All goods subject to Section 232 tariffs — whether in full or derivatives. Note: for derivative products, the derivative is excluded but the non-derivative component remains subject to Section 122

• Goods made in Canada or Mexico whether they are eligible for USMCA or not.

• Articles of textiles or apparel produced in Costa Rica, the Dominican Republic, El Salvador, Guatemala, Honduras, or Nicaragua

Full exclusion details: Annex I | Annex II

File Pending Entries BEFORE Section 122 Kicks In

This is time-sensitive.

If you have goods sitting in a bonded warehouse, or goods arriving before February 28 that were loaded onto a vessel before February 24, file your entries tomorrow.

Under the exclusion window, those goods qualify for neither IEEPA nor Section 122.

For goods entering today: do not hold off hoping to avoid the IEEPA. File now. The IEEPA tariff you pay today will most probably be refunded once the CIT rules. Section 122, on the other hand, is not going anywhere.

IEEPA Refunds

The Court of International Trade (CIT) still has to rule for the next steps now that the supreme court has ruled against IEEPA, but previously, CIT has denied an injunction to stop CBP from liquidating entries, with the promise that refunds will not be blocked even if entries are liquidated before a final ruling on the legality of the IEEPA tariff. Which means that refunds are almost certainly coming.

You can read the ruling here: CIT Ruling No. 25-154

What You Need to Do – Action Items

We cannot file Post Summary Corrections yet , we are waiting on the CIT’s ruling. But that does not mean you sit and wait. Here is what you can do right now:

Action 1: Set Up Your ACE Account

Every importer that plans to collect a refund needs an ACE (Automated Commercial Environment) account with CBP. If you do not have one, sign up now, it is relatively straightforward.

Need help? Download our ACE tutorial:

⚠️ Important: When entering your EIN in ACE, add two zeros after your EIN number. It will look like this: 11-111111100

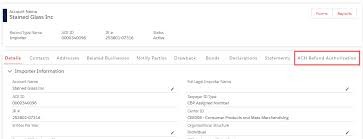

Once enrolled, navigate to the ACH Refund page (image below) and enter your banking details for direct deposit. This is how CBP will pay your refund directly into your account, and you will be able to track the status of each refund request online.

Action 2: Confirm Your Broker Can Handle Refund FilingsNot all customs brokers are prepared to process the volume and complexity of Post Summary Corrections for IEEPA refunds. Reach out to your broker now and ask directly. If they cannot handle it, the time to find someone who can is before the filings open, not after. We are currently accepting a limited number of new clients for refund filing support. Reach out to us and if we cannot help directly, we will connect you with the right industry experts. Action 3: Review Your Compliance Record FirstThis is the uncomfortable one, but it needs to be said. Before you file a refund request, take an honest look at your entry history. Go through your invoice values, country of origin declarations, and HTS classifications. If any of these were done incorrectly – intentionally or not – filing a refund request could expose you to litigation and audit risk. Here is how we suggest you think about it:

For importers with significant compliance concerns, we strongly urge you to speak with a trade attorney before filing. Options like prior disclosure exist and can significantly reduce your exposure. Do not try to navigate this alone. Refund Eligibility — A Few Key Reminders

What We Are Doing for Our ClientsFor existing clients: we have already been filing entries strategically to get goods cleared under the IEEPA where possible, ensuring you are positioned for refunds rather than locked into Section 122. We are making all necessary arrangements to be ready the moment the CIT rules and Post Summary Corrections can be filed. We will work with each of you directly on your refund filings. For prospective clients: we are accepting a limited number of new clients for refund filing support. This is one of those moments where you realize that working with a partner who knows what they are doing, and has your back, matters more than just the cheapest ocean freight rate. If you have been thinking about making a change, now is the time to reach out. Questions? Ready to get started on your refund filings? Reach out. This blogpost is for informational purposes only and does not constitute legal advice. Consult with a licensed trade attorney for guidance specific to your situation. |